Are your clients exploring captives, and could they be missing out? With more businesses embracing self-insurance models, retail agents must understand where captives shine and where excess & surplus (E&S) expertise fills the gaps. Learn how CRC helps retail agents build better towers and stay competitive in a shifting market.

Captive insurance is surging in popularity, especially among large insureds seeking more control, transparency, and long-term cost savings in the face of economic volatility, rate pressure, and claims unpredictability. CRC Specialty brokers help retail agents retain accounts with creative structuring and fill the gaps where traditional and captive markets fall short. A well-placed buffer layer or excess solution can mean the difference between a retained client and a lost opportunity in today’s environment.

WHY CAPTIVES? AND WHY NOW?

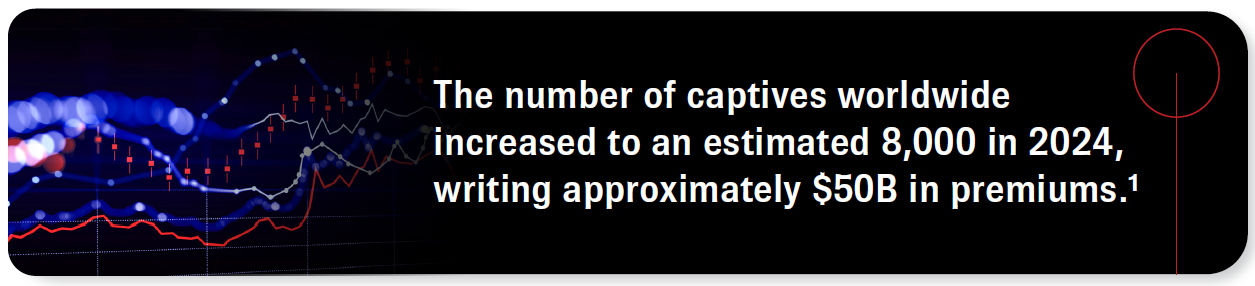

Captives are self-insurance vehicles formed by businesses or groups of companies to insure their risks. These programs give insureds greater transparency and control over claims handling, loss prevention, and cost allocation. Over time, successful captive participants may even see returns on unused loss funds.

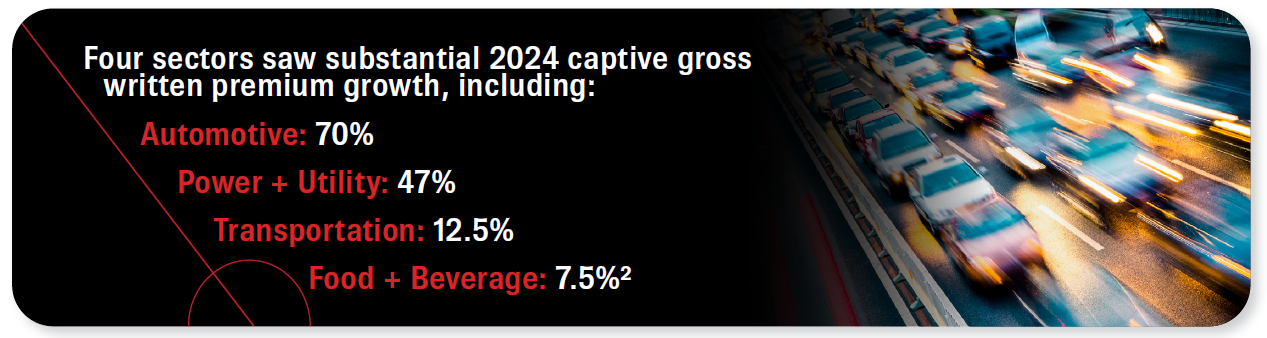

In the past, captives were considered too complex for middle-market accounts, often reserved for billion-dollar corporations. But today, group captives and rent-a-captive structures have opened the door to middle-market players, especially those with annual revenues over $50M. Industries like construction, manufacturing, security, transportation, real estate, and staffing show increased interest. Driving this momentum are several key factors:

- More volatile traditional insurance pricing

- Insured dissatisfaction with claims service

- Tax incentives and better loss cost predictability

- Increased education and captive management access

Retail agents who ignore this trend risk losing relevance — and their best clients.

WHERE CAPTIVES FALL SHORT

While captives provide control and stability, they also create new complexities. They typically require excess coverage, reinsurance support, or specific placements to round out a program. Here’s where CRC adds value:

- Buffer Layers + Lead Access

Captives often retain a large portion of risk including the first $1M or $2M in loss. However, standard carriers aren’t always eager to attach directly above these layers, especially in distressed industries or lead excess positions. That’s where buffer layers come into play. CRC brokers regularly place $1M x $1M or $2M x $1M auto buffer and general liability buffer layers to bridge the gap between a captive and the rest of the tower. With access to a deep bench of E&S markets and proprietary facilities, CRC can structure responsive, affordable layers that allow carriers to attach where they’re most comfortable. These buffers are especially critical for accounts with larger fleets, where auto losses lead to increased severity, particularly in high-hazard sectors of the construction, manufacturing, distribution, or transportation industries. In many of these classes, CRC brokers have built full towers over captives, creating complete and competitive structures without reliance on admitted markets. - Excess Tower Structuring

When captives are part of the program, brokers must manually build the entire tower, making a wholesale broker’s role even more vital. Many traditional carriers are no longer willing to offer large limits or lead positions, resulting in more quota share solutions, layered placements, and creative stacking using multiple markets.

CRC’s e3 platform enables brokers to quickly combine capacity from multiple carriers, often assembling $10M–$15M towers in days, not weeks. While e3 doesn’t typically quote directly over a captive, it can attach just above and provide retailers the flexibility to meet client demands and pricing pressure.

With capacity tightening in specific sectors, particularly in excess auto and large construction, retailers who can’t access these tools are losing out to those who can. - Filling Gaps Created by Changing Market Appetite

Even captive participants are feeling the ripple effects of market shifts. Capacity pullbacks, increased attachment points, and selective underwriting mean more gaps at renewal. CRC Specialty brokers are adept at identifying where standard or incumbent carriers are backing away and filling those voids quickly.

By staying close to evolving underwriting trends, wholesale brokers also help agents future-proof programs. When carriers change appetite mid-term, CRC Specialty is ready with alternatives that help protect continuity and retain accounts.

DON’T WAIT FOR COMPETITOR TO OFFER A CAPTIVE FIRST

CRC brokers are increasingly observing a trend in which retail clients transition to working with new agents, not due to pricing issues, but because the new agent offers a captive structure that their current retail agency partner does not.

Retailers who delay in presenting captive options may find themselves at a disadvantage if a competitor approaches a client. This is why CRC Specialty brokers actively collaborate with agents to explore potential captive opportunities, even when the current structure is traditional.

KEY TAKEAWAY: THE CAPTIVE + E&S COMBO IS THE FUTURE

The growing adoption of captives isn’t a threat to the E&S market; it’s an evolution. Captives and E&S placements create hybrid structures that give insureds more power, agents more options, and brokers a new frontier of opportunity.

CRC Specialty brokers are helping build smart, layered, and compliant programs that protect clients while preserving flexibility. By leveraging the wholesale market’s reach and proprietary tools like Insurisk’s exclusive e3 product, agents gain the firepower to serve captive clients at the highest level.

BOTTOM LINE

Captives are growing fast, and they’re here to stay. But even the best captive programs need excess support, buffer layers, and creative structuring. CRC Specialty helps retail agents fill those gaps, build better towers, and stay one step ahead of the competition.

Don’t let someone else offer the solution first. Bring Team CRC with you. Contact your CRC Specialty producer today.

CONTRIBUTORS

- Jeff Dunn has over 30 years of insurance industry experience and is a Senior Casualty Broker with CRC Atlanta.

- Ryland Fisher has over 7 years of insurance industry experience and is an Associate Casualty Broker with CRC Atlanta.

END NOTES

- 2024 Captive Growth Exceeds Expectations, Captives Insure, January 7, 2025. https://captives.insure/insights/2024-captive-growth

- Captives Expand Risk Portfolios and Premium Volume in 2024, Risk & Insurance, July 2, 2025. https://riskandinsurance.com/captives-expand-risk-portfolios-and-premium-volume-in-2024/