Is construction casualty finally stabilizing, or are hidden risks still reshaping the market? From nuclear verdicts and litigation funding to inflation pressures and the surge of new capacity, contractors face both challenges and opportunities. What does this mean for your business, and how can you prepare for what’s next?

At the end of 2025, the construction casualty market continued its slow march toward stabilization after the hardening years of 2020-2022. Expanding competition, particularly from MGA capacity and start-up insurers, has created improved outcomes for insureds in favorable venues with strong loss records. However, distressed accounts remain challenged on both the primary and lead excess sides, where rate relief remains elusive.

Claims costs, social inflation, and inconsistent settlements continue to shape carrier strategies, leaving insureds, retail agents, and brokers navigating a marketplace where stabilization does not necessarily mean ease. The result is a complex balance: competitive forces pushing down rates for some while ongoing loss trends push them upward for others.

NUCLEAR VERDICTS

The impact of nuclear verdicts, whether defined as $10M+ awards or any verdict far exceeding expectations, remains profound. Social inflation, anti-corporate sentiment, and aggressive plaintiff strategies have fueled settlements that reshape actuarial assumptions. Insurers are refining claims handling, but “shock losses” are increasingly routine, forcing brokers and insureds to adapt risk financing strategies.

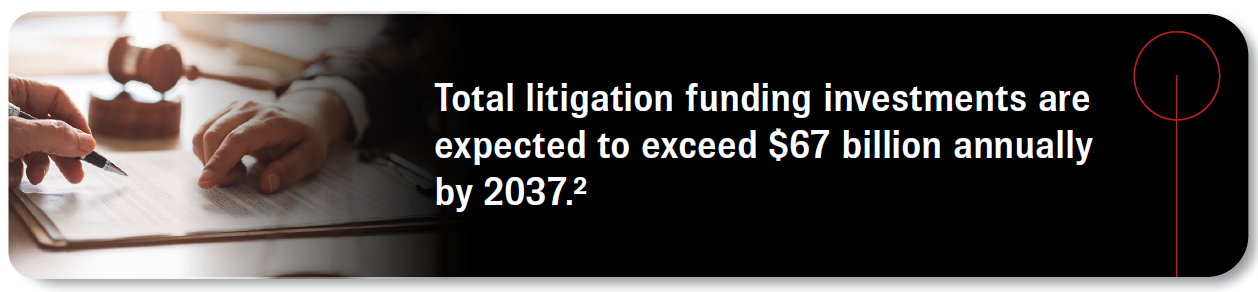

THIRD-PARTY LITIGATION FUNDING

The growth of litigation financing has made lawsuits a new asset class. Outside investors fund plaintiff litigation in exchange for large portions of settlements. This trend raises defense costs, extends timelines, and adds uncertainty to outcomes. Carriers may react with reduced approved counsel panels or, worse, shifting defense obligations to insureds.

CLAIMS HANDLING CONCERNS

To pay or not to pay? Clients increasingly question why carriers settle, not just whether they will. Quick settlements meant to avoid jury trials often frustrate insureds and create misalignment with their carrier partner. In response, more insureds are exploring SIR placements, corridor retentions, and direct claims control. On the other hand, some of the largest settlements often involve multiple carriers with several hesitant to pay their full limit. These delays, in the face of what may seem like an imminent judgement to an insured, can impact the insured’s ability to bid for work. This dynamic requires brokers and agents to guide clients toward structures that balance protection with influence.

NEW CAPACITY

New carriers and MGAs are aggressively pursuing construction risks. While this adds short-term competition and rate stabilization, unproven claims departments present uncertainty. Excess markets may adjust terms or pricing depending on their view of underlying carriers. Brokers and agents should proactively educate clients and insureds on claims handling track records, especially for new capacity, and guide clients toward partners with proven reliability.

LATENT DEFECT CLAIMS

Projects from the 2010–2019 soft market era, especially urban condo developments, are showing late-stage defect claims. This long-tail exposure is weighing on portfolios and reminding the market of the need for disciplined underwriting even during robust construction cycles.

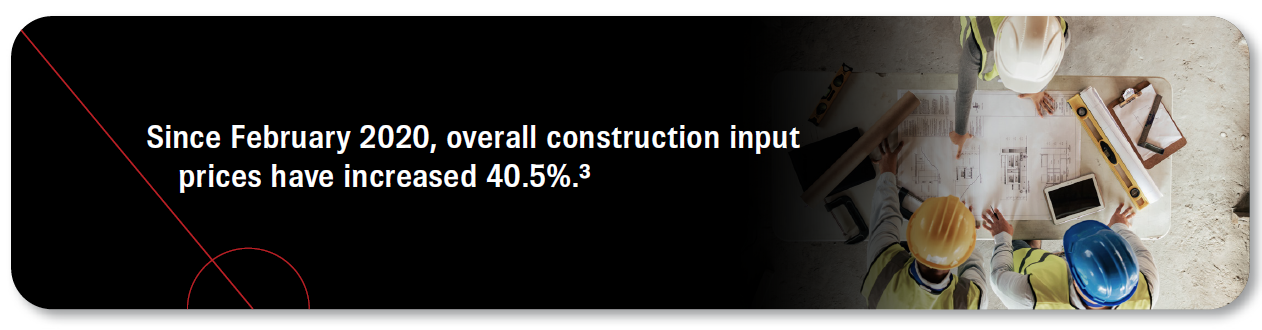

INFLATION IMPACTS

Inflation continues to hit both sides of the carrier ledger. Carriers must pay today’s higher claims costs with yesterday’s premium dollars, while rising interest rates provide offsetting investment yield. Court backlogs further extend settlement timelines, enhancing the value of float.

For insureds, however, inflation pressures budgets, creating resistance to rising premiums. This friction between carrier needs and client willingness will drive renewal displacement. Brokers who can help insureds model retention options, restructure towers, and align coverage with cost are critical.

E&S CHANNEL GROWTH

The E&S market continues to expand and was projected to hit $147 billion in 2025.1 Yet profitability remains uneven, as evidenced by the sector’s 107% combined ratio in 2020. Progress has been made with combined ratios in the upper 80s in both 2023 and 2024, but stability remains far from certain.

For construction insureds, E&S growth means more placement options, but not necessarily better terms. Brokers must help clients weigh the promise of new markets against the risks of immature claims practices and inconsistent underwriting discipline.

GOVERNMENT + ECONOMIC FORCES

Macroeconomic and regulatory influences also shape construction risks:

- Government Spending: Shifts in contract allocation could impact timing and demand in the infrastructure sector.

- Tariffs + Trade Wars: Material costs remain sensitive to global dynamics, with potential to slow project starts.

- Infrastructure Needs: Aging systems, from power to water and roads, still require investment, supporting civil construction demand.

Together, these forces create a backdrop of opportunity tempered by volatility.

GUIDANCE FOR CLIENTS

In today’s transitioning environment, insureds must answer a key question: “What are you willing to pay, and how much, to secure consistency of carrier, claims, and coverage?” Some clients will choose disruption, experimenting with added higher retentions, excess structures, or new carriers to reduce premiums. Others will prioritize stability and accept higher costs to maintain established partnerships. Brokers play a critical role in helping clients evaluate these tradeoffs and prepare for continued volatility in claims, capacity, and economic factors.

BOTTOM LINE

CRC Specialty brings unmatched expertise, scale, and market access to the construction sector. Our producers understand the nuances of casualty volatility, from nuclear verdicts to emerging MGA capacity. We provide:

- Depth of Relationships: Access to the broadest array of markets, including proven and emerging players.

- Claims Insight: Guidance on navigating settlement strategies, claims handling differences, and retention structures.

- Specialized Expertise: Dedicated construction specialists with deep industry knowledge.

- Problem-Solving Approach: Innovative program design tailored to client needs in volatile environments.

What makes CRC different is our ability to combine specialized knowledge, trusted relationships, and unmatched market leverage to deliver stability and opportunity, even in uncertain times.

CONTRIBUTORS

- Evan Aldrich is Office President for Charleston, South Carolina, and CRC Specialty’s National Construction Practice Director.

- Andrew Grim is a Senior Vice President with CRC’s National Construction Practice. He is located in Dallas, Texas.

END NOTES

- WSIA’s Kelley: Surplus Lines Premium Volume Poised to Hit $147 Billion in 2025, E&S Insurer, September 14, 2025. https://www.theinsurer.com/e-and-s/news/wsias-kelley-surplus-lines-premium-volume-poised-to-hit-147-billion-in-2025-2025-09-14/?utm_source=Sailthru&utm_medium=Alert&utm_campaign=E-and-S-Insurer-Alert&utm_term=091425

- Beneath the Surface: A Deeper Dive Into Third-Party Litigation Funding, Washington Legal Foundation, August 4, 2025. https://www.wlf.org/2025/08/04/publishing/beneath-the-surface-a-deeper-dive-into-third-party-litigation-funding/

- Construction Material Prices Rose in January, Says BLS, Engineering News Record, February 13, 2025. https://www.enr.com/articles/60308-construction-material-prices-rose-in-january-says-bls#:~:text=On%20a%20yearly%20basis%2C%20construction,the%20first%20half%20of%202025.%E2%80%9D