Many insureds assume their Employee Benefits Liability (EBL) endorsement covers all benefit-related risks, but does it really? We unpack the crucial differences between EBL and Fiduciary Liability and explain why both are essential in today’s environment.

As employee benefits programs evolve and regulatory scrutiny increases, understanding how these coverages work together is essential. Retail agents who can clearly articulate those differences deliver real value and protect both their clients and themselves.

DEFINING THE BASICS

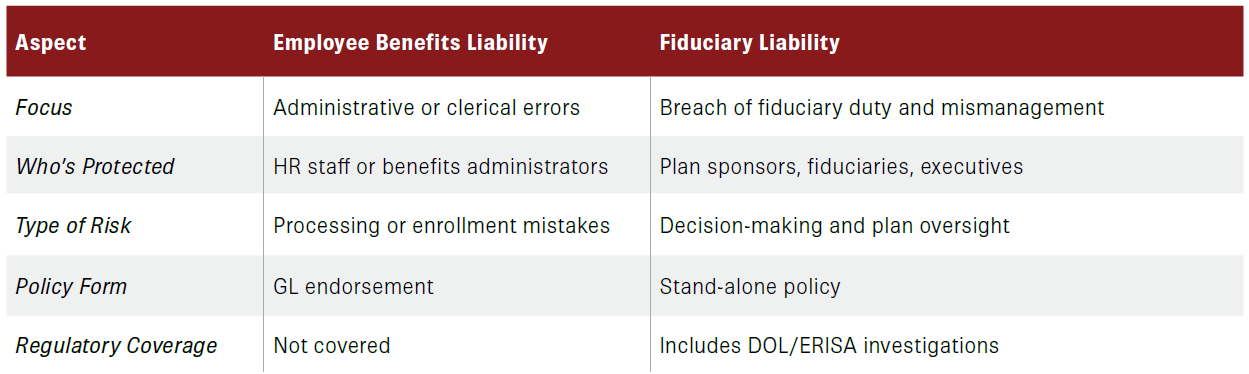

Employee Benefits Liability (EBL) coverage is most often added as an endorsement to a General Liability policy. It provides protection against administrative errors or omissions in handling employee benefits, such as failing to enroll an employee, processing the wrong coverage level, or omitting a dependent.

EBL policies are typically claims-made with low sublimits, designed to address clerical missteps rather than strategic or fiduciary decisions.

By contrast, Fiduciary Liability is a stand-alone policy that protects plan sponsors, fiduciaries, and administrators under the Employee Retirement Income Security Act (ERISA). It covers breaches of fiduciary duty, mismanagement of plan assets, and failures to act in the best interest of plan participants, often including defense costs and regulatory investigations. A Fiduciary Liability policy is much broader than EBL. Fiduciary coverage protects against breaches of duty and administrative errors, offering a more complete safety net.

EBL VS. FIDUCIARY: THE CORE DIFFERENCES

EBL covers the HR-level mistakes — things like forgetting to enroll someone in a health plan. Fiduciary Liability extends further, protecting the people making decisions about how plans are managed or investments are handled.

COMMON MISCONCEPTIONS

Confusion around these coverages is widespread. Three myths consistently surface:

“We already have EBL, so we don’t need Fiduciary.”

- EBL only covers administrative errors. It does not address ERISA violations, investment decisions, or breaches of fiduciary duty. A Fiduciary Liability policy is required for that.

“Fiduciary Liability is only for large corporations.”

- Small and mid-size businesses also carry fiduciary risk if they offer benefits such as 401(k)s, HSAs, or ESOPs. Anyone with decision-making power over plan assets can be held personally liable.

“We outsource our benefits administration, so we’re not at risk.”

- Outsourcing does not remove fiduciary exposure. Employers may still face claims for imprudent vendor selection or failure to properly oversee third-party administrators.

WHY BOTH COVERAGES MATTER

EBL and Fiduciary Liability are complementary, not interchangeable. Both play essential roles in comprehensive protection. EBL policies often exclude key exposures:

- ERISA violations

- Dishonest or fraudulent acts

- Investment errors or poor performance

- Fines and penalties from regulatory bodies like HIPAA or HITECH

By contrast, strong Fiduciary Liability policies often include sublimits (sometimes $250,000 or more) for regulatory penalties and coverage for voluntary correction programs with the Department of Labor. These benefits are not found in EBL.

The best Fiduciary Liability policies even cover defense costs for allegations of dishonesty until a final adjudication is made. That kind of protection simply doesn’t exist under an EBL endorsement.

EMERGING TRENDS AND EVOLVING RISKS

The Fiduciary Liability landscape continues to change. Several emerging concerns driving demand for coverage include:

- Excessive fee litigation around 401(k) and 403(b) plans has intensified underwriting scrutiny.

- Cybersecurity exposures are increasingly relevant as benefit plan data becomes a target.

- Vendor management claims are rising as employers are held responsible for third-party administrator mistakes.

- Expanding benefit offerings such as HSAs, ESOPs, and wellness programs broaden fiduciary responsibility.

CLAIMS SCENARIOS

Scenario 1: The Missed Enrollment

An HR manager forgets to enroll a new employee in the company’s health plan. When that employee later faces uncovered medical expenses, the company faces an EBL claim.

Scenario 2: The Investment Oversight

A company’s retirement plan committee is accused of allowing excessive management fees and failing to diversify investments. Plan participants file a class-action lawsuit against the fiduciaries. This falls under Fiduciary Liability, not EBL.

Together, these examples show how each policy plays a distinct but vital role in a comprehensive risk management strategy.

WHAT AGENTS NEED TO KNOW

Understanding and explaining these differences can set retail agents apart. Agents can add value to their client relationships with a proactive approach.

- Ask the right questions: Identify who makes benefits decisions and whether they’re aware of their fiduciary responsibilities.

- Educate proactively: Share examples that illustrate both administrative and fiduciary risks.

- Highlight personal liability: Fiduciary responsibility can extend to individuals, not just the organization.

Agents who know how to talk about EBL and Fiduciary Liability coverage are offering more than a product. They’re providing true advisory value. It’s also a way to protect agents from E&O exposure if a client ever faces an uncovered claim.

BOTTOM LINE

At CRC Specialty we understand that one size doesn’t fit all. We combine market access, deep expertise, and consultative support to help retail agents secure the right mix of coverage for every client.

CRC Specialty’s advantage lies in:

- Specialist guidance on nuanced executive liability exposures, from ESOPs to cybersecurity.

- Tailored program design that closes coverage gaps and ensures regulatory readiness.

- Trusted carrier relationships providing access to broad, flexible fiduciary and EBL options.

When retail agents partner with CRC, they gain more than a wholesaler. They gain a strategic partner committed to helping them and their clients move faster and go further. Reach out today.

CONTRIBUTORS

- Allyson Benda, Senior Broker, of CRC Nashville has over 20 years of experience in the insurance industry, all dedicated to Management and Professional Liability lines of business. She is an active member of the ExecPro Practice Group.

- Katie Smith, Broker, has more than 10 years of industry experience dedicated to Management and Professional Liability lines. She is part of CRC Seattle and a member of the ExecPro Practice Group.