With Builders Risk rates softening and capacity expanding, there’s a window of opportunity, but the market remains complex. Interest rates, construction starts, material inflation, and lender expectations vary regionally. Learn why CRC’s Insurisk Builders Risk+ offers the precision and capacity to meet today’s challenges.

Builders who had to contend with soaring insurance rates, higher deductibles, and reduced insurance coverage during the hard property market have seen more flexibility in 2025. Rates have eased from late-2023 peaks, with some carriers lowering prices to win business, though overall pricing has largely stabilized.

While insurers may now offer more flexibility in some areas, the underlying construction environment continues to shape risk appetites and pricing strategies. In addition, understanding where and how new projects are breaking ground, along with the economic factors influencing those starts, is critical to anticipating market behavior. This makes it essential to look at current construction activity and regional trends driving demand.

CONSTRUCTION ACTIVITY + REGIONAL TRENDS

While the Builders Risk insurance environment is improving, building costs remain elevated. ENR’s Q1 2025 cost report shows that the Materials Cost Index rose 3% year-over-year. The Building Cost Index increased 1.6%, while the Construction Cost Index climbed 0.9%.1 These indicators confirm that expenses remain high, even if inflation is moderating. Lumber prices have started to come down after significant highs earlier in the year, but overall material inflation and tariff impacts, particularly on technology and materials imported for large-scale projects, continue to weigh on budgets. Contractors also face uncertainty around interest rates, which remain elevated, and ongoing labor shortages and higher wages that drive up total project costs.

Construction starts in the first half of 2025 showed mixed results. Total construction starts were up 1% from the same period in 2024, with nonresidential starts up 6%, residential starts down 5% and nonbuilding starts up 1%.10 Year over year, total construction starts were up 4% from the 12 months ending June 2024, with residential starts down 1%, nonresidential starts up 8% and nonbuilding starts up 3%.10

Infrastructure projects steadily increased, while demand in commercial sectors like office space and retail has declined.9 On the other hand, there continues to be strong demand for multifamily housing. Rates for podium and garden-style ground-up multifamily projects have moderated, despite recent large wood frame construction fires that caused tens of millions in losses.5, 6, 7 In California, the massive Los Angeles area wildfires will likely lead to higher property insurance rates, and rebuilding demand may spur higher building and material costs.

Multifamily completions reached unprecedented national levels in 2024 - over 590,000 units, mainly concentrated across Sun Belt metros like Dallas–Fort Worth (approx. 35,400 deliveries), Atlanta (24,134), and Phoenix (26,216).3 Sun Belt markets, home to 13 of the top 20 metro areas with the most starts, dominated multifamily deliveries in 2024, while units permitted per capita in markets like Tampa and Orlando remained among the highest in the nation, even as overall permitting declined from pandemic-era highs. On a year-to-date basis through June, multifamily starts were up 8.1% with Southeast growth continuing, and Texas holding firm as the number one state for multifamily starts.4 These regional patterns and project types directly influence insurer appetite. Carriers are adjusting their strategies to stay competitive while managing risk. This balance between demand and risk tolerance is evident in the evolution of capacity and pricing.

CAPACITY + PRICING

A wave of capacity established during the hard market has left hungry carriers with growing budgets competing over fewer opportunities. At the same time, experience indicates that these rates are likely not sustainable in the long term. While this competitive environment creates opportunities for insureds, it also raises the question of whether today’s pricing will prove durable if construction activity remains sluggish and input costs stay elevated.

In general, insurance appetite has broadened. Insurers offer larger lines (often $10M - $30M or more) and more competitive rates. However, carriers usually still require high wind/water deductibles. Many carriers also require 5% wind deductibles across Florida, even in northern Florida or more inland areas that previously saw more flexibility. Convective storms and wind/ hail remain contentious points for most carriers. The need for excess wind/hail coverage is becoming more prevalent, along with the push for increased deductibles higher than the AOP deductible on convective storm-exposed locations.

Carriers may also be more willing to write extensions and offer preferred terms, which had become difficult and expensive in recent years. Increases on extension terms have come down significantly, and in many cases, new projects can secure 90-day rate-locked extensions. While renovation placements (e.g., office conversions, subsidized housing) remain complex, underwriting appetite has improved as long as submissions include detailed reports from structural engineers when adding stories to an existing structure, replacing elevators, moving load-bearing walls, or replacing roofs. Projects where the percentage of the existing structure is more than the percentage of complex renovation may present an obstacle for underwriting.

UNDERWRITING DYNAMICS

The essential information for any wholesale Builders Risk submission should include, at a minimum:

- Completed application including General Contractor info

- Line-item budget

- Detailed project schedule (Gantt Chart)

- Geotech and soils report

- Site plan

In addition, clients with experience in subsidized housing or frame and renovation projects should be aware of specific project requirements. Depending on the project and the location, underwriters may also seek information about crime scores in urban areas considered risky and site security plans. Some insurers had previously insisted on hiring from a short list of pre-approved security vendors, but those lists now include far more vendors. Instead of pre-screened vendors, insurers may simply require that vendors meet a specified list of requirements.

Due to the threat of fire and water damage, insurers may also want to see fire and water damage prevention plans. Builders should be prepared to provide contractors’ hot work permits. Hurricane response plans may also be necessary for Tier 1 wind areas in Florida. Accounts with better quality assurance, quality control, and loss prevention standards receive preferential treatment. Accounts that do not specifically outline loss prevention plans and actions around wildfire, water damage, and hurricane preparedness are typically required to develop those practices to obtain coverage.

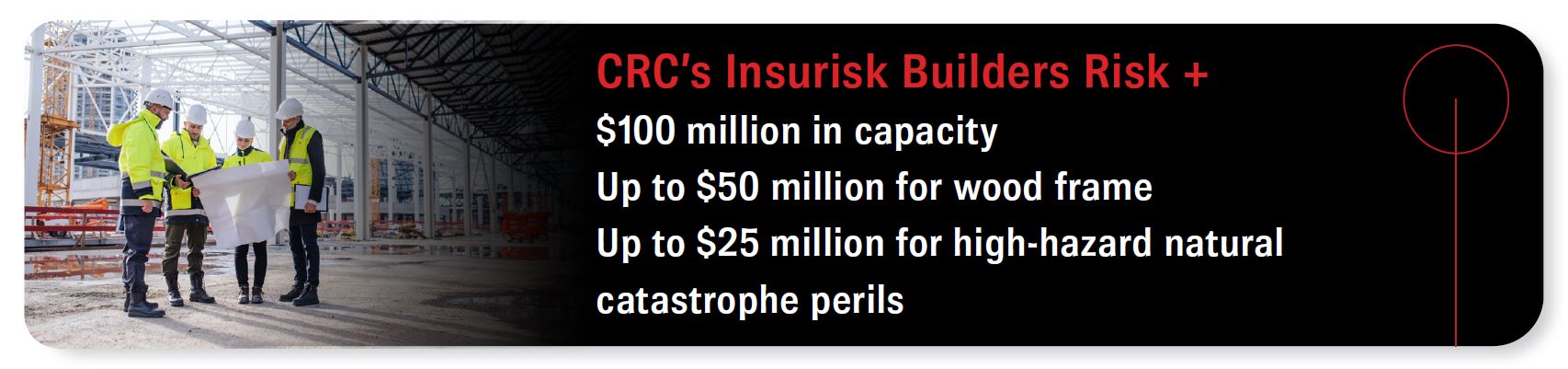

While underwriting requirements have become more detailed, these measures strengthen project submissions and help secure favorable terms. However, even with strong documentation, coverage gaps and capacity challenges can still arise, especially for complex, multi-location, or high-hazard projects. This is where CRC’s exclusive Insurisk Builders Risk + product stands out, offering enhanced flexibility, higher limits, and tailored solutions designed to meet the evolving needs of today’s construction market.

BOTTOM LINE

Though the Builders Risk insurance market has warmed considerably in 2025, navigating it requires more than pricing comparisons. Elevated material and labor costs, lingering tariff impacts, and uncertainty around interest rates continue to challenge project feasibility. With construction slowing in some sectors and carriers aggressively competing for limited opportunities, today’s softer pricing may not hold. Partnering with the right wholesale broker is critical to securing reliable coverage today and preparing for the next turn in the cycle.

The CRC Specialty team brings deep expertise and exclusive access to Insurisk Builders Risk +, enabling agents to craft tailored programs with firm limits, smooth underwriting, and flexibility for lender demands. The result? Clients receive smarter protection, better pricing, and coverage that matches the complexity of today’s construction environment.

Reach out to your CRC Specialty broker today.

CONTRIBUTORS

Colin McLean is a Senior Broker and Builders Risk Specialist with CRC Atlanta.Randy VanHorn is a Property Broker with CRC Group’s Philadelphia, PA, office.Philip Young is a Property Broker with CRC’s Birmingham, AL, office.END NOTES

- Q 2025 Cost Report: Growth for Some Materials Prices in 2024, Engineering NewsRecord, February 26, 2025. https://www.enr.com/articles/60363-1q-2025-cost-report-growth-for-some-materials-prices-in-2024#:~:text=The%20ENR%2020%2Dcity%20average,0.9%25%20over%20the%20same%20period.

- Construction Analytics Outlook 2025,” Ed Zarenski, February 5, 2025. https://edzarenski.com/2025/02/05/construction-analytics-outlook-2025/

- Sun Belt Oversupply Strategy: Navigate New Deliveries,” The Guarantors, June 2025. https://www.theguarantors.com/blog/owners-and-operators/sun-belt-oversupply-strategy-navigate-new-deliveries

- Multifamily starts spike for 5-plus units in June Multifamily Dive, July 2025. https://www.multifamilydive.com/news/apartment-starts-multifamily-completions-new-construction/753730/#:~:text=Dive%20Brief:,month%2Dover%2Dmonth%20decline.

- Fire destroys under-construction apartment complex in Cleveland Heights, Jan. 25, 2025, Cleveland.com, https://www.cleveland.com/news/2025/01/fire-ravages-marquee-at-cedar-lee-apartments-under-construction.html

- Here’s what we know about the $155 million Redwood City housing project that burned in a massive fire, ABC7News, June 4, 2024. https://abc7news.com/post/155m-redwood-city-affordable-housing-project-destroyed-massive/14910599/

- Plans underway to rebuild Las Vegas apartment complex destroyed in large fire, Feb. 5, 2025, KTNV. https://www.ktnv.com/news/plans-underway-to-rebuild-las-vegas-apartment-complex-destroyed-in-large-fire

- LA wildfires by the numbers: insured losses, total losses, ratings, rates. Claims Journal, Jan. 24, 2025. https://www.claimsjournal.com/news/national/2025/01/24/328611.htm

- Construction Starts Pull back 10% in July, Dodge Construction Network, August 22, 2025. https://www.construction.com/company-news/construction-starts-pull-back-10-in-july/#:~:text=For%20the%2012%20months%20ending%20July%202025%2C%20total%20residential%20starts,South%20Central%20and%20South%20Atlantic.&text=Dodge%20Construction%20Network%20ha

- The Construction Broadsheet, Dodge: June Construction Starts Up 16%, July 22, 2025. https://theconstructionbroadsheet.com/dodge-june-construction-starts-up-p2067-174.htm#:~:text=1%2C%202025%2C%20through%20June%2030,projects%20to%20break%20ground%20were